What are Yearn Vaults? ETH Vault Explained

So what are Yearn Vaults all about? Also, how does the ETH Vault work under the hood and how can it bring over 60% returns? We’ll go through all of this in this article.

Yearn Vaults

Okay, one more thing before we start. If you’re new to the Yearn protocol or if you need a quick recap you can check my other article on Yearn and the YFI token here.

Cool, let’s start with the Vaults.

Yearn Vaults, in essence, are pools of funds with an associated strategy for maximising returns on the asset in the vault. Vault strategies are more active than just lending out coins like in the standard Yearn protocol. In fact, most vault strategies can do multiple things to maximise the returns. This can involve supplying collateral and borrowing other assets such as stable coins, providing liquidity and collecting trading fees or farming other tokens and selling them for profit. Each vault follows a strategy that is voted in by the Yearn community.

Yearn Vaults were created as a direct response to yield farming and liquidity mining that made searching for the highest yield much more complex than just switching between different lending protocols. You can learn more about yield farming and liquidity mining here.

Similarly to the standard Yearn protocol, when tokens are deposited to a vault the user receives their corresponding yTokens that can be redeemed for the underlying tokens.

One of the important rules when it comes to Vaults or Yearn protocol, in general, is the fact that you always withdraw the same asset that was initially deposited. So farmed tokens and accrued fees are sold for the main asset in the vault. The amount that is withdrawn is the initial amount that was put in, plus the pool yield that was earned, minus the fees.

Not everything that is deposited into a vault is put in a strategy. The vaults differentiate between vault holdings and strategy holdings. Most of the funds are used by an active strategy, but there is also an idle amount that just sits in the vault.

When a user withdrawals from a vault, the funds first come from the idle portion of the vault and there is no withdrawal fee charged. If there are not enough funds in the idle portion of the vault to cover the withdrawal, the funds have to be withdrawn from the strategy which results in a 0.5% fee.

On top of that, some profit-earning transactions will result in a 5% fee to subsidize the gas costs. For community-made strategies such as the ETH strategy, currently, 10% of this fee goes to the strategy creator. So creating new vault strategies can be a good opportunity for a skilled developer.

Fees that don’t go to the strategy creator end up in a dedicated treasury contract. If the money in the treasury contract exceeds the $500k threshold, everything over that amount is redirected to the governance staking contract.

There are currently multiple Yearn Vaults available such as stable coin vaults: DAI, TUSD, USDC, USDT; Curve LP vaults: y, busd, sbtc; Non-stable assets: LINK, YFI, ETH.

ETH Vault

Now, let’s have a look at the Yearn ETH Vault (yETH) to understand the concept of Vault strategies better.

As we mentioned earlier, a strategy for each Vault is chosen by the community. We’re focusing on the current running strategy for the yETH vault that may and will most likely change over time.

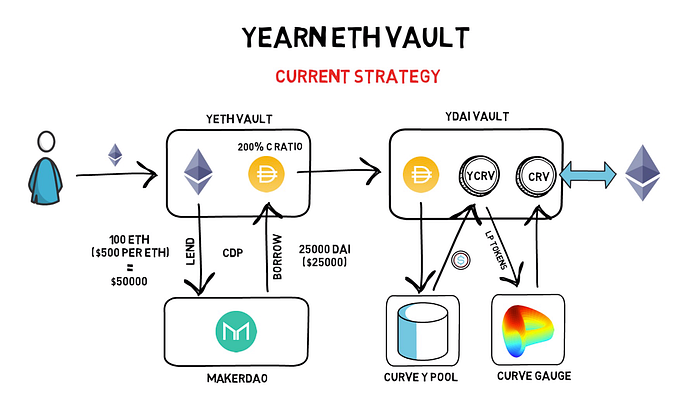

In the current strategy after a user deposits ETH into the Vault, the ETH is put into a MakerDAO lending platform as collateral. By supplying ETH collateral to MakerDAO the ETH strategy can borrow DAI at 200% collateralization ratio, creating a collateralised debt position (CDP). This means that if 100 ETH was put into the MakerDAO with $500 per ETH, the strategy could borrow up to $25,000 DAI.

Borrowed DAI is then put into the Yearn DAI Vault that uses a strategy that deposits DAI to Curve’s Y pool that is a pool with stable coins consisting of DAI, USDC, USDT and TUSD. Now, because of the current liquidity mining program of the Curve’s CRV token, providing liquidity to the Curve’s pools and locking LP tokens in the Curve Gauge result in getting rewarded with extra CRV tokens, on top of standard trading fees generated by just supplying liquidity to a pool.

The ETH strategy then periodically sells CRV tokens for ETH and uses the accrued trading fees from the Y liquidity pool to accrue even more interest.

These steps all put together can, at the moment, result in high returns of around 60% on your ETH deposited to the yETH Vault.

Two days after launching, the yETH Vault had already reached 370,000 ETH locked in the Vault and it became the largest CDPs on MakerDAO. Further deposits to the yETH vault were also temporarily halted to balance between best profits and best risk adjustment.

yETH Vault has a great potential of sucking in more and more ETH and becoming pretty much a black hole for ETH. This should, in theory, increase the price of ETH as more and more ETH is taken out of circulation.

Is that 60% in the yETH Vault sustainable? Probably not, it all depends on the current liquidity mining programs available. If there are no more programs, like CURVE’s CRV one, available or rather there is no interest in the programs so the farmed tokens are not worth anything, the return on the Vault would go down, most likely to a single-digit or low double-digit APY.

One of the most important benefits of using Vaults is automating your yield farming.

Yield farming can be a pretty time-consuming and expensive activity, so if you’re not willing to spend hours searching for the best yield farming opportunity, spend hundreds of dollars in gas fees to move funds around and keep monitoring your collateralization ratio, it is probably better to rely on the Vaults.

Risks

This all sounds pretty cool, but let’s not forget about potential risks.

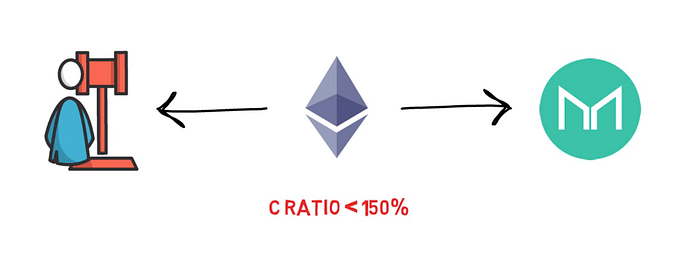

Besides our standard DeFi risks such as smart contract bugs and stable coins losing their peg to the dollar, the ETH deposited as collateral on MakerDAO is susceptible to liquidation if the collateralization ratio falls below 150%.

In our previous example, if the ETH price drops below $375 the collateralization ratio would drop below 150%. If this happens the ETH Vault would have 1 hour to bring the collateralization ratio back to over 150%. The reason for this is that MakerDAO’s Oracle Security Module (OSM) gives the CDP owners 1 hour to put more collateral in before being liquidated. The ETH Vault is directly integrated with this module, so it can react to changes in price ahead of time by bringing back the collateralization ratio to around 200% every time the ETH price drops.

Summary

Yearn Vaults are clearly one of the most interesting new developments in the DeFi space, but like with pretty much everything else in DeFi, before deciding to use a particular protocol always make sure to understand the associated risks.

So what do you think about Yearn Vaults and the ETH Vault in particular? Do you think it will suck up a lot of circulating ETH causing the price to go up?

If you enjoyed reading this article you can also check out Finematics on Youtube and Twitter.

Originally published at https://finematics.com on May 9, 2020.